The terms payment orchestration and payment processing are often conflated across fintech marketing, vendor documentation, and even internal product discussions. For a PayTech firm at the early stages of building its stack, this ambiguity is harmless enough. For an electronic money institution (EMI), payment institution (PI), or neobank that is scaling across multiple payment rails, multiple jurisdictions, and multiple product lines, mixing the two is an architectural mistake that compounds over time.

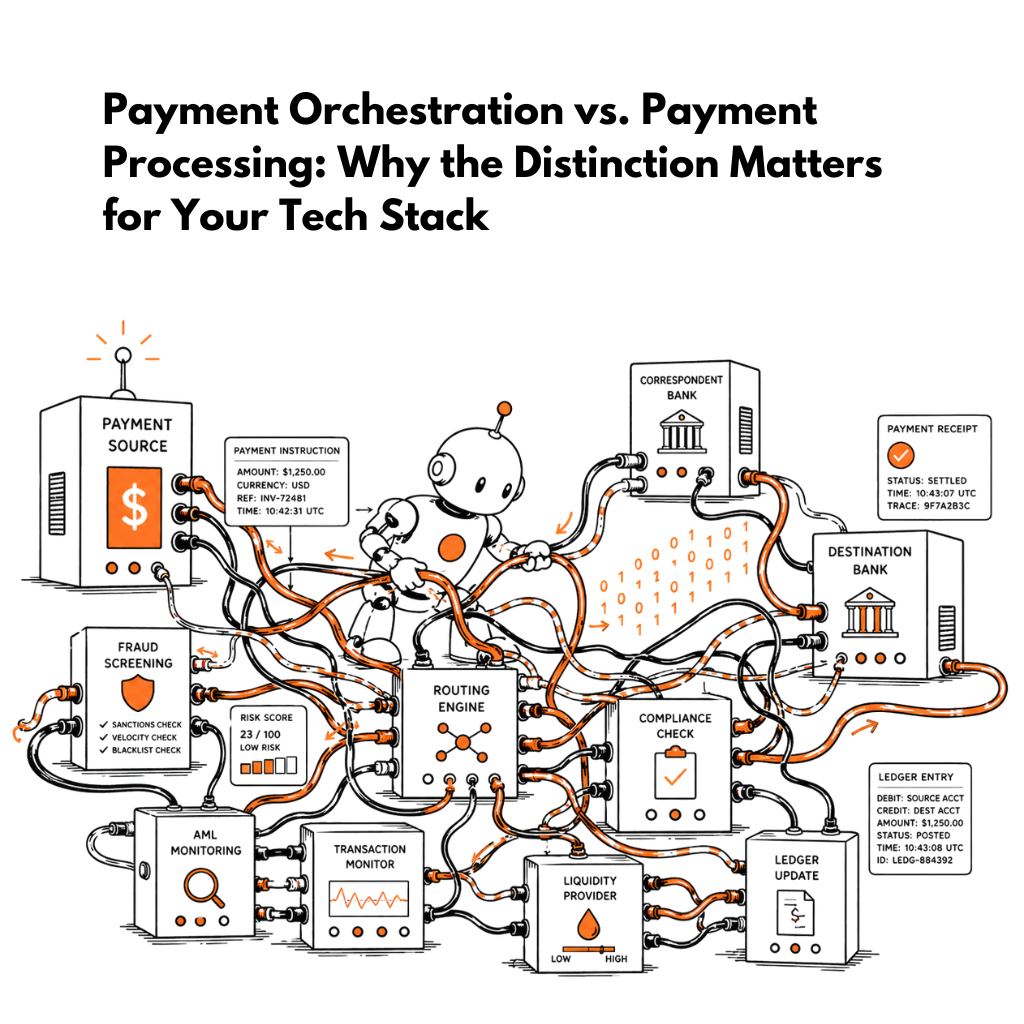

Payment processing is the execution of a single payment instruction: validate, screen, debit, route, confirm. Payment orchestration is the layer above that decides which processing path to invoke, when, and why, across a portfolio of payment rails, correspondent banks, schemes, and instrument types. The distinction is not academic; it determines where logic lives in your platform, who owns it, and what happens when something goes wrong at scale.

For PayTechs operating across SEPA Credit Transfer, SEPA Instant, SWIFT, Faster Payments, Bacs, Chaps, Fedwire, OCT, and increasingly USDC or stablecoin rails, payment orchestration is not an optional enhancement. It is the operational logic that sits between your customers’ payment intent and the settlement infrastructure that moves funds. Without it, you accumulate routing rules scattered across databases, manual overrides that become undocumented institutional knowledge, and a reconciliation problem that grows with every new rail you add.

In this article, we examine what payment orchestration actually means in a regulated PayTech context, what it requires from your core infrastructure, and how its connection to compliance, reconciliation, and multi-rail logic determines whether your payment stack can scale or simply accumulates technical debt.

- Part One: What Is Payment Orchestration and Why Does the Distinction With Payment Processing Matter?

- Part Two: What Payment Orchestration Actually Requires From Your Core Infrastructure

- Part Three: How Payment Orchestration Connects to Reconciliation, Reporting, and Multi-Rail Logic

- Baseella's Approach: Payment Orchestration as a Core Platform Capability

Part One: What Is Payment Orchestration and Why Does the Distinction With Payment Processing Matter?

What does payment processing actually mean in a regulated context?

Payment processing, in the context of a regulated EMI or PI, is the end-to-end sequence of operations that executes a single payment instruction from initiation to settlement confirmation. That sequence typically covers: authentication and authorisation of the payment request, balance and limit checks against the payer’s account, compliance screening (sanctions, PEP, adverse media, transaction risk scoring), accounting entries (debit the payer, credit the outbound settlement position, debit fees, etc.), dispatch to the correspondent bank or payment scheme, and receipt of a settlement confirmation that triggers the final ledger update.

In a well-designed payment platform, these steps happen in a defined, auditable sequence for every transaction. Payment processing is deterministic: given the same inputs, it produces the same outputs. It is the machine that executes a single instruction correctly.

What payment processing does not do is decide which banking partner to send the instruction to, or whether to split it, retry it on a different rail if the first fails, apply a cost-based routing preference, or hold it for a compliance review window before release. Those decisions are not processing. They are orchestration.

What does payment orchestration add – and what does it not replace?

Payment orchestration is the decision layer that governs how payment instructions are routed before they enter the processing pipeline. It determines, based on a defined set of rules and live conditions, which processing path a payment should follow. In a multi-rail environment, that might mean choosing between SEPA Instant and SEPA Credit Transfer based on SEPA Instant reachability, urgency and cost thresholds, falling back to a secondary partner bank if a primary route is unavailable, applying jurisdiction-specific handling for payments crossing regulatory borders, or flagging a payment for manual review before routing based on an elevated risk score.

Payment orchestration does not replace payment processing; it precedes it and, in some architectures, supervises it. The orchestration layer makes the routing decision. The processing layer executes it. A robust payment orchestration system makes that handoff explicit, auditable, and recoverable, so that when a routing decision produces an unexpected outcome, you can trace exactly what logic was applied, with what inputs, at what timestamp.

This distinction becomes consequential when a payment fails. If orchestration and processing are collapsed into a single opaque flow, a failure is simply a failed payment. If they are distinct, a failure carries a machine-readable reason: the routing logic selected rail A, rail A returned a timeout at step three of processing, the orchestration layer retried on rail B, and B confirmed settlement. That trace is the difference between a support ticket resolved in minutes and one investigated across three systems for half a day.

Why does the boundary between the two matter operationally?

For a PayTech with a single partner bank and a single payment rail, the boundary between payment orchestration and payment processing is largely irrelevant. The routing decision is always the same: use the one available path. The distinction becomes unavoidable the moment you add a second rail, a second correspondent, two virtual IBAN issuers, lack of liquidity with a preferred partner bank, etc.

At that point, routing logic must be explicitly defined somewhere. The question is not whether payment orchestration exists in your stack (it always has to) but whether it is intentionally designed, centrally managed, and connected to the data it needs to make good decisions, or whether it is distributed across configuration tables, hardcoded exception handlers, and undocumented manual interventions.

PayTechs that treat payment orchestration as a configurable platform capability from early in their build avoid the more painful alternative: a growing collection of rail-specific processing scripts that each embed their own routing assumptions, with no unified view of what is happening across the payment book at any given moment. The operational cost of the latter becomes measurable precisely when you need to add a new rail quickly or explain your routing logic to an auditor.

Part Two: What Payment Orchestration Actually Requires From Your Core Infrastructure

What data does payment orchestration need, and where does it live?

Effective payment orchestration is a data problem before it is a logic problem. The routing decisions that matter, such as which rail to use, whether to hold a payment, whether to apply a fallback, depend on real-time access to a set of data points that span multiple functional domains within a payment platform.

A routing decision at the point of payment initiation may require: the payer’s current account/e-wallet balance and credit limits, the live risk score assigned to the transaction by the scoring engine, the beneficiary’s screening status (cleared, flagged, or pending), the current operational status of each available payment rail and correspondent, the payment’s currency, amount, available liquidity, and destination jurisdiction, and applicable fee or FX logic that affects cost-based routing preferences.

None of this data originates in the orchestration layer. It lives in the accounts module, the scoring engine, the compliance database, the treasury position, and the rail connectivity layer. Payment orchestration that is designed as an isolated microservice or third-party tool must retrieve all of this via API calls, introducing exactly the latency, dependency risk, and data exposure concerns that apply to composable compliance tooling. Each external call is a potential point of failure on the critical payment path.

Payment orchestration that runs natively within the core platform resolves this differently – with direct access to the same databases that hold balance, risk, and compliance data. Routing decisions can be made in-process, consulting live internal state, without crossing a network boundary. The result is faster routing resolution, no additional external dependency, and no secondary data transfer to a third-party orchestration vendor.

What happens when orchestration logic sits outside the core?

Many PayTechs, particularly those assembling composable stacks, deploy a dedicated payment orchestration layer as a standalone service that sits between the customer-facing API and the downstream processing and connectivity components. This architecture has surface-level appeal: it appears modular, it can be deployed and updated independently, and it maps to the composable banking narrative of best-in-class specialists for each function.

In live operations, external payment orchestration creates a set of predictable problems. First, it requires a synchronous data retrieval step before every routing decision: balance from the core, risk score from the scoring engine, and rail status from a connectivity monitor. Each of which introduces latency and a failure dependency. If the orchestration service cannot retrieve a data point, it must either block the payment or proceed with incomplete information. Neither is acceptable for a regulated institution processing payments under strict schemes’ timing requirements.

Second, external payment orchestration produces a split audit trail. The routing decision is logged in the orchestration system. The accounting entries are logged in the core ledger. The compliance screening result is logged in the AML/CTF platform. Reconstructing the full story of a payment from initiation through routing decision, through processing, and through settlement requires correlating records across three or more systems. In a regulatory review or incident investigation, that correlation is your responsibility, and it is rarely straightforward.

Third, updating routing logic in an external payment orchestration service typically requires a deployment cycle, vendor coordination, or at minimum a configuration change in a system that your operations team does not own end-to-end. For a PayTech that needs to respond quickly to a correspondent bank outage, a scheme rule change, or a compliance directive, that delay is an operational liability.

How does routing logic interact with compliance at the point of execution?

This is the intersection that payment orchestration vendor marketing typically underemphasises. Routing is not a neutral operation; it is a regulated one. Under PSD2 Article 78 and its national transpositions, payment service providers must execute payment transactions in accordance with the unique identifier and the consent provided by the payer. Under the EBA’s Guidelines on the Security of Internet Payments, institutions must apply transaction monitoring and risk scoring before authorisation, not after routing.

This creates a sequencing requirement: compliance must precede routing, because routing decisions may themselves depend on compliance outputs. A high-risk-score transaction may be routed to a manual review queue rather than dispatched immediately. A payment to a newly flagged beneficiary may be held pending case management review. A transaction that triggers a transaction monitoring alert mid-processing may need to be intercepted before the correspondent bank call is made.

Payment orchestration that is architecturally separated from the compliance layer cannot enforce this sequencing reliably without explicit integration work. The compliance result must be returned to the orchestration layer before the routing decision is finalised. If those two systems are loosely coupled, there is a brief timing window in which a routing decision could theoretically be made before all compliance signals are resolved. That window may be acceptable in some architectures. In a regulated payment institution, it is an audit finding waiting to happen.

Part Three: How Payment Orchestration Connects to Reconciliation, Reporting, and Multi-Rail Logic

What is multi-rail payment processing and why does it create an orchestration problem?

A multi-rail payment environment is one in which a PayTech has connectivity to more than one payment infrastructure, for example, SEPA Credit Transfer alongside Target 2, Chaps alongside Faster Payments, or fiat rails alongside blockchain-based settlement for crypto-asset transactions. Multi-rail capability is increasingly a baseline expectation for regulated EMIs and PIs that serve international clients or operate across multiple EEA markets.

Multi-rail connectivity creates an immediate payment orchestration requirement. For any given payment instruction, there may now be multiple valid processing paths. The routing decision must be made consistently, correctly, and in alignment with the client’s service configuration. Without an explicit payment orchestration layer, that decision defaults to hardcoded logic, manual selection, or first-available routing, none of which is appropriate for a regulated institution required to apply defined execution policies and document them.

The complexity compounds with each rail added. A PayTech with three partner banks and four active payment schemes has a routing matrix that cannot be managed manually at volume. Payment orchestration is the only scalable answer, whether embedded in the core platform or deployed as a configurable rules engine. The architecture question is simply where that engine lives and what data it can access.

How does reconciliation break when orchestration is disconnected from the ledger?

Reconciliation is the process of confirming that every payment instruction dispatched by your platform has a corresponding settlement confirmation from the correspondent bank or scheme, and that both match the accounting entries posted in your ledger. In a single-rail environment, reconciliation is relatively tractable: one outbound batch, one settlement file, one matching exercise.

In a multi-rail environment with separate payment orchestration, reconciliation becomes structurally more complex. The orchestration layer knows which rail was selected for each payment. The ledger knows what accounting entries were posted. The correspondent connectivity layer knows what was actually dispatched and what was confirmed. If these three systems do not share a common payment reference throughout the lifecycle, reconciliation requires a join across system-specific identifiers: a fragile operation that breaks whenever a retry, a fallback routing, or a split payment creates a non-one-to-one mapping between orchestration records and settlement confirmations.

The consequence is an exception rate that grows with volume. Payments that settle on a fallback rail have a different correspondent reference than the one recorded at orchestration time. Retried payments may generate duplicate settlement events that must be manually matched. Each exception requires a human to cross-reference two or three systems to determine the actual payment status. For a PayTech processing tens of thousands of payments per day, an exception rate of even 0.1% represents a significant daily operational burden.

Payment orchestration embedded in the core platform (where routing decisions, accounting entries, correspondent calls, and settlement confirmations all flow through connected modules on a shared payment identifier) eliminates this class of reconciliation problem by design. There is no join to perform because there is no seam.

What do regulators expect from your payment routing audit trail?

Regulators evaluating a PayTech’s payment operations are interested in more than whether payments settle correctly. Under the EU’s Digital Operational Resilience Act (DORA), in force since January 2025, in-scope payment and e-money institutions must be able to demonstrate end-to-end traceability of payment operations and the ICT systems supporting them. Under the FCA’s PS21/3 on Operational Resilience, UK firms must map and test the technology dependencies underpinning their important business services, which for a PayTech includes the payment routing function.

In practice, this means a regulator or auditor can reasonably ask: for a given payment instruction, what routing logic was applied, what data inputs were used, what rail was selected and why, what happened when that rail returned an error, and what the full timeline of the payment lifecycle looks like from initiation to settlement. If payment orchestration lives in a separate system with its own logs, answering that question requires you to produce a coherent narrative from fragmented records across multiple vendor portals.

For a PayTech that has experienced a payment routing incident (a period of elevated failure rates, a mis-routed batch, or a compliance hold that delayed a significant volume of payments) translates into the inability to produce a clean audit trail in a regulatory review. Payment orchestration that is integrated with the core platform and shares its audit logging infrastructure produces that trail natively, without reconstruction.

Baseella’s Approach: Payment Orchestration as a Core Platform Capability

The architectural argument above reflects a deliberate design philosophy at Baseella. Payment orchestration is not a module bolted onto a lean core; it is embedded within the payment processing pipeline, drawing on the same internal services – the Accounts module for balance and limit data, the Scoring module for real-time risk signals, the Block lists module for compliance status, Transaction processing rules for payment orchestration, Transactions module for ledger entries that execute the payment itself.

When a payment instruction enters the Baseella platform, the routing decision is resolved by consulting internal state via GraphQL Federation, which fans out parallel queries to each relevant subgraph (i.e., balance, risk score, compliance flags, rail availability, liquidity availability, processing rules) and receives all responses before the routing decision is finalised. This happens inside the platform boundary, without external API calls on the routing path, and within milliseconds rather than in the hundreds of milliseconds that sequential external calls would introduce.

The payment processing or, in other words, orchestration rules configured by the client, which rails are active for which payment types, which risk thresholds trigger a hold, which currencies route via which correspondents, what fee logic applies, are maintained directly within the platform by the client’s operations team without requiring a deployment cycle or vendor involvement. Routing configuration is a business operation, not an engineering task.

The result for reconciliation is that every payment in Baseella carries a single persistent payment identifier from initiation through routing through processing through settlement confirmation. There is no join across systems to reconstruct a payment’s lifecycle. The audit trail that a regulator would request in a DORA review or an FCA resilience assessment is the same trail that the operations team uses to investigate a support query. It is a single record, in one platform, with a complete and chronologically ordered event log.

For PayTechs evaluating whether to build, buy, or assemble payment orchestration capability, the diagnostic questions are the same ones that apply to compliance tooling: how many external calls does your routing decision require per payment, whose infrastructure does payment data transit through during orchestration, how would you produce a complete payment routing audit trail on 48 hours’ notice, and what happens to your routing logic when one of your correspondent banks experiences a degradation event. The answers to those questions are more revealing than any feature comparison.

Baseella is a core banking and payments platform built for electronic money institutions, payment institutions, neobanks, money service businesses, and crypto-asset service providers. To see how Baseella handles payment orchestration, multi-rail connectivity, compliance, and reconciliation in a single integrated platform, visit Baseella online or schedule a demo.